By Tom Rivers, Editor Posted 7 February 2026 at 8:55 pm

Aaron D’Angelo

SHELBY – A 36-year-old Medina man has been charged with murder and attempted murder after two brothers were stabbed today in Shelby.

Aaron D’Angelo allegedly caused the death of Dale R. Lang, 65, who was pronounced deceased at the scene, 4643 South Gravel Road (Route 63).

His brother John Lang, 67, also suffered multiple stab wounds and was transported to Medina Memorial Hospital and then Erie County Medical Center. His condition is currently unknown, Sheriff Chris Bourke stated in a press release sent at about 8:30 p.m.

The Orleans County Sheriff’s Office responded to a reported 911 disturbance at the above address at 11:55 a.m.

Upon arrival, Bourke said a Sheriff’s deputy encountered D’Angelo, who was armed with a knife and confronted the deputy. The deputy deployed a Taser, successfully subduing D’Angelo, who was then taken into custody without further incident, Bourke said.

As additional personnel arrived on scene, Dale Lang and John Lang were discovered inside the residence with multiple stab wounds.

D’Angelo has been charged with the following offenses:

Murder in the Second Degree (Class A-I Felony)

Attempted Murder in the Second Degree (Class B Felony)

Assault in the First Degree (Class B Felony)

Menacing a Police Officer (Class D Felony)

Criminal Possession of a Weapon in the Fourth Degree (Class A Misdemeanor)

He is currently being held at the Orleans County Jail pending arraignment.

The Orleans County Sheriff’s Office was assisted at the scene by the Medina Police Department, Medina Ambulance, the Shelby Fire Department, and the New York State Police Forensic Identification Unit.

“This incident remains under investigation,” Bourke said. “Anyone with information related to this incident is encouraged to contact the Orleans County Sheriff’s Office.”

By Tom Rivers, Editor Posted 7 February 2026 at 3:29 pm

SHELBY – A person has died and another seriously injured after two stabbings in Shelby at 4643 South Gravel Rd.

Another man, who allegedly stabbed the other two individuals, is in custody, Sheriff Chris Bourke said.

Law enforcement was dispatched to scene at 11:55 a.m. for report of a disturbance in Shelby Center. The responding deputy encountered an aggressive individual who was covered in blood, Bourke said. The man came at the deputy, who used a taser to try to subdue the man, the sheriff said.

That man remained aggressive, but was able to be put in the back of the police car. He is being interviewed by law enforcement and is now being cooperative, Bourke said.

There were two people inside the house and one was dead from stabbing wounds. Another man suffered more than 20 stabbing wounds, and remains alive but with severe injuries, Bourke said.

The man was transported to Medina Memorial Hospital and then transferred to Erie County Medical Center by ambulance due to mercy Flight being unable to fly its helicopter due to the weather conditions.

Law enforcement remain on scene to process the evidence. Route 63 has been closed between Alabama Road and Oak Street.

The sheriff said a news release will be forthcoming with more details.

‘Job Corps is one of the best bang-for-your-buck programs we have to boost our local economies’

Press Release, U.S. Senate Minority Leader Charles Schumer

Photo by Tom Rivers: This sign on Route 63 in Shelby notes the Iroquois Job Corps. This center has space for up to 225 students who are served by 104 full-time equivalent employees.

After Schumer stood at Job Corps centers across Upstate NY to lead the fight to protect one of the nation’s largest and most effective workforce training programs from Trump’s effort to eliminate it, U.S. Senator Chuck Schumer today announced he has successfully preserved funding for Job Corps and helping students across America, including thousands in New York, get the skills they need to enter in-demand careers.

“Job Corps is one of the best bang-for-your-buck programs we have to boost our local economies, which is why I fought hard to protect it from Trump’s proposed cuts,” said Senator Schumer. “I’m proud to announce that, following my advocacy, we have preserved funding for Job Corps, ensuring the continuation of one of America’s largest and most effective workforce training programs.”

The just-passed Fiscal Year 2026 Labor, Health and Human Services, Education funding bill rejects Trump’s call to eliminate Job Corps and instead provides $1.76 billion in federal funding to keep them open. Schumer also secured language that blocks the closure of Job Corps Centers unless such closures meet specific requirements.

Anand Vimalassery, National Job Corps Association Interim President & CEO said, “Job Corps faced unprecedented disruption and uncertainty over the last year. Through it all, Senator Schumer stood by our students and staff in Calicoon, Cassadaga, Glenmont, Medina, New York City, and Oneonta. His leadership is helping ensure young adults in New York continue to have a pathway into the skilled workforce through Job Corps and we’re grateful for his support.”

In May 2025, Trump paused operations at Job Corps centers nationwide. Afterward, a federal judge temporarily blocked Trump from shutting down Job Corps centers, and another federal judge said operations must resume until the previous case is resolved. Schumer explained that the Trump administration not only attempted to shut down Job Corps centers, but in his budget request, Trump said he wanted to totally zero out funding for the program, effectively killing the program without needing the approval of federal courts.

After hearing about Trump’s proposed cuts, Schumer last year traveled to Job Corps centers across Upstate New York, from the Iroquois Job Corps center in Orleans County to the Cassadaga Job Corps center in Chautauqua County and the Otsego Job Corps Center, to stand with students, staff, and small business owners and demand we protect this vital pipeline for skilled workers to fill jobs.

In addition to fighting back on Trump’s proposed elimination of funds for Jobs Corps in the Fiscal Year 2026 appropriations bill, Schumer led efforts in the Senate to oppose the Trump administration’s destructive and potentially illegal actions like pausing existing funds for the Job Corps centers.

Schumer called on U.S. Department of Labor Secretary Lori Chavez-DeRemer to protect Job Corps and demanded answers on these destructive efforts. Thanks to Schumer’s leadership, the Fiscal Year 2026 Labor, Health and Human Services, Education funding bill rejects Trump’s call to eliminate Job Corps and instead provides $1.76 billion in federal funding – which is consistent with the previous year – to keep them open and includes language to protect against Trump’s efforts to illegally shut down specific centers.

“The Iroquois Job Corps Center has been a cornerstone of opportunity in Orleans County for more than sixty years, helping young people gain the skills and credentials they need to succeed while strengthening our local economy,” said Lynne Johnson, Chairman of the Orleans County Legislature. “Preserving funding for Job Corps is critical for our students, our workforce, and our community. Thanks to Senator Schumer, the Iroquois Job Corps Center can continue delivering real pathways to good-paying careers and supporting the next generation of skilled workers.”

Schumer said Job Corps centers have helped millions of young people ages 16 to 24 finish high school, learn technical skills, and get jobs in in-demand fields such as healthcare and construction. Low-income and at-risk young people have received stable housing and healthcare while developing the skills they need to get good-paying jobs after graduation. Across Upstate NY, centers in Albany, Sullivan, Orleans, Otsego, and Chautauqua Counties serve thousands of young New Yorkers and employ over 500 staff.

By Tom Rivers, Editor Posted 3 February 2026 at 11:17 am

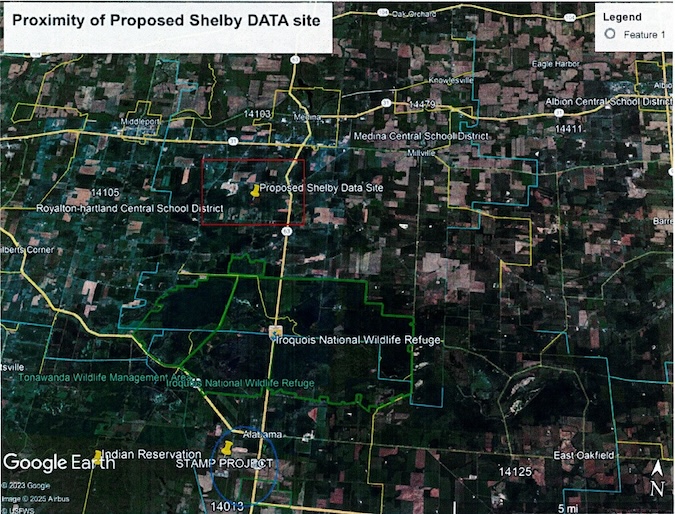

Genesee would receive $285 million in revenue over 30 years, plus an estimated $18 million in sales tax annually to be split by county and state

Photos by Tom Rivers: Stream U.S. Data Centers held an open house at the Alabama Fire Hall on Monday evening for people to meet members of the development team for the data center. Many of the attendees are concerned about the environmental impacts on the community, including the nearby wildlife refuge and Tonawanda Indian Nation.

ALABAMA – A massive data center proposed for the STAMP site in Alabama, just a few miles south of Orleans County, would bring a major influx of revenue for Genesee County, said officials at the Genesee County Economic Development Center.

Stream U.S. Data Centers would pay $285 million over 30 years to Genesee County, the Town of Alabama and Oakfield-Alabama Center School. (The project also would receive $744 million in tax incentives. The GCEDC board is expected to accept an application from Stream during its board meeting on Thursday. There will be public hearings about the incentives and the site plan for the data center.)

Bradley Wells, site selection and development manager for Stream U.S. Data Centers, speaks to reporters at Monday’s meeting. He said the project uses a relatively small footprint of the STAMP site and won’t generate much traffic after construction. The data center would have 125 employees working different shifts. There would be about 1,000 people working on construction of the data center’s three buildings, each over 700,000 square feet.

The company also will have to pay sales tax on its electricity usage and that is expected to be about $18 million a year to be split by Genesee County and the state.

Stream U.S. Data Centers is proposing to invest over $11 billion in the data center at STAMP. GCEDC gets a fee when it facilitates a project, usually 1.25 percent of the development costs.

With the data center, the fee would be 0.75 percent or about $83 million. That money would help build out public water in Genesee County and with infrastructure at other GCEDC business parks, said Mark Masse, GCEDC president and CEO. Five of the eight GCEDC parks are currently fully occupied but there is space at STAMP, Le Roy and in the Pembroke parks.

“This whole program is generational revenue for Genesee County,” Masse said during an interview on Monday during an informational meeting by Stream at the Alabama fire hall.

The project is outside Orleans County, but Masse and GCEDC officials expect Orleans would see significant benefit for employment and other services for the data center, as well as people looking to move into the community.

The project has faced resistance from Orleans County, including Legislature Chairwoman Lynne Johnson who doesn’t want any wastewater from STAMP to go into the Oak Orchard Creek, which is a major tourism draw for fishing in the county.

STAMP will be using the Village of Oakfield sewer plant for treatment, and Masse said the plant will be upgraded to treat phosphorus.

The Allies of Tonawanda Seneca Nation have been vocal in opposition of the data center, saying it uses enormous amounts of electricity – 500 megawatts – that could impact electricity rates for other customers.

The Allies passed out flyers listing concerns with noise, impacts to wildlife, water usage and pollution, air pollution, e-waste, and other environmental impacts.

Arthur Barnes of Shelby was among the attendees at Monday’s meeting. He wore a “Stop STAMP” button. Barnes would have preferred to hear a presentation from the developer to the group, but instead Stream had people meet one on one or in small groups. Barnes said the presentation was “too slick” and didn’t consider the impacts of the project on the community.

Bradley Wells, site selection and development manager for Stream, said the meeting format was a chance to “have one on one time with developer.”

The new data center would be “unique and premium in the market,” he told reporters at the meeting.

The data center helps meet a need with the “growth of internet, growth of interconnectivity, subscription streaming and artificial intelligence,” he said.

The STAMP site is attractive for Stream because it offers all of the existing infrastructure –with electricity, water and waste water. Wells said the facility would use “very minimal water” and would operate on a closed loop air cooling system.

There are very restrictive noise requirements, and Wells said the site would operate at 65 decibels at day and 45 decibels at night from the Stream property lines. The noise would be quieter farther away from the site. Wells said 65 decibels is similar to the sound when talking in a room and 45 decibels is the sound of a quiet office environment.

Stream U.S. Data Centers showed renderings of how a vacant field at STAMP could be turned into a large data center.

The company, based in Dallas, Texas, will need to get through an environmental review with the GCEDC the lead agency. The Allies of the Seneca Nation, Orleans County and others wanted the state Department of Environmental Conservation to lead that review. Barnes said the GCEDC role “is like the fox guarding the hen house.”

Wells said Stream strives to build a long-lasting partnership with the community. The company is hopeful construction could start in 2026 with the facility to begin operations in 2027, although a full buildout is expected to take until 2030.

He foresees “1,000 continuous trade jobs” during the construction. Once that is complete, the traffic impact from the data center would be “extremely low,” Wells said, with 125 employees working different shifts, many of them software specialists and engineering technicians.

Other manufacturing at STAMP could see many more employees and deliveries, with a much bigger impact on traffic in the community, he said.

Stream would operate on 90 acres out the 1,250 acres at STAMP.

“We think it’s one of the most dense, best uses of the park right now,” Wells said.

By Tom Rivers, Editor Posted 27 January 2026 at 8:54 pm

Retired DA Joe Cardone pitches his property in Shelby for massive project

File photo by Tom Rivers: A massive data center, totaling 2.2 million square feet, could be headed to the STAMP site off Route 63 in the town of Alabama.

ALABAMA – The leader of the Orleans County Legislature is asking the state Department of Environmental Conservation to be the lead agency for an environmental review of a proposed data center at the STAMP site in Alabama, just south of Orleans County.

Lynne Johnson, chairwoman of the County Legislature, said in her Jan. 16 letter that the Genesee County Economic Development Center would be “biased” in the review of Project Double Reed and it would be better to have the environmental impact review conducted by the state Department of Environmental Conservation, not the GCEDC. Johnson sent the letter to DEC Commissioner Amanda Lefton.

GCEDC has fired back with its own letter to the commissioner and also Regional Director Timothy Walsh, claiming the Orleans opposition is based on “sour grapes” because Orleans wanted the project in Shelby, not Genesee County.

GCEDC also said Orleans has been unable to secure larger-scale projects and tried to thwart Genesee County from running a sewer transmission line from STAMP to Oak Orchard Creek in Shelby to derail development of STAMP. GCEDC has decided to use the sewer plant in Oakfield, with the discharged water still ultimately going into the Oak Orchard.

Adam S. Walters of the Phillips Lytle LLP law firm sent the letter on behalf of the GCEDC on Monday, and cited several procedural errors in Johnson’s letter that should make it invalid. Among the five cited: the letter wasn’t sent by certified mail or other form of receipted delivery (instead by email).

The letter also didn’t have the backing of the full legislature because there was no formal resolution from the County Legislature, Walters said.

Orleans County also isn’t an “involved agency” for for the proposed data center as it “will not fund, approve or directly undertake Project Double Reed,” Wash writes. GCEDC considers Orleans County as an “interested agency” due to STAMP’s proximity to the Orleans/Genesee County line and sewer infrastructure planned to run from STAMP into Orleans County.

Walters said that Johnson’s letter “has no effect” since the GCEDC staked its claim to serve as lead agency more than 30 days ago and that “the NYSDEC itself did not challenge GCEDC’s declaration of intent.”

“It appears that the objections in the Johnson Letter do not stem from any legitimate environmental concerns but rather result from GCEDC refusing to push Project Double Reed to locate in Orleans County rather than at STAMP,” Walters said.

GCEDC first stated it would be lead agency for Project Double Read about a year ago. At the time the $6.3 billion project was proposed at 900,000 square feet and it would have paid $218.4 million to municipalities in revenue over 20 years. The data center now is proposed to be more than double that initial plan.

The initial declaration by GCEDC to be lead agency in the environmental review was rescinded when the project changed to a 2.2 million-square-foot data center consisting of three two-story buildings. It would be on approximately 90 acres at STAMP with another 40 acres to be utilized as temporary construction/logistics areas.

Johnson, in her letter, said no businesses are currently operating at STAMP despite years of public investment in the site. (Edwards Vacuum is building a 250,000-square-foot manufacturing site at STAMP, a $319 million project that is part of the semi-conductor industry.)

“Under GCEDC’s stewardship, STAMP has been nothing more than a series of unfulfilled promises, questionable allocation of resources and a series of environmental pollution events so significant that this Agency and the Federal government revoked its permits,” Johnson said.

GCEDC holds a “biased position,” Johnson said, to “justify the fact that it has spent almost $500 million of taxpayer dollars is to jump start a project — any project — regardless of its environmental impact.”

Her letter said the data center would have a negative impact on air quality, energy usage, water usage and wastewater disposal.

GCEDC responded that Johnson is way off on claiming $500 million in taxpayer dollars for STAMP. The number represents the total investment so far at the site, and most of that has been private contributions, GCEDC said.

“Accordingly, the motivations for Orleans County’s objection appear to be based on so called ‘sour grapes’ regarding failed efforts to secure a multi-billion dollar project and past litigation defeats rather than an honest concern about GCEDC serving as lead agency,” Walters wrote in his letter.

Joe Cardone has proposed his 284 acres of land off Route 63 in Shelby be considered for a large-scale data center.

Walters, the GCEDC attorney, said Johnson’s letter may be an effort to steer the data center into Orleans County. Joe Cardone, the retired district attorney for Orleans, met with the GCEDC on December 18 to pitch his property for the data center. Walters said Cardone is trying to “poach” the project so it can be on his property.

GCEDC, in its letter to the DEC officials, included information provided by Cardone to the GCEDC on why he sees his site as a superior location.

Cardone said it would be away from the Tonawanda Indian Reservation and the wildlife management areas, sensitive sites that many detractors say make STAMP a bad fit for such a large development project.

Cardone, in his presentation to GCEDC, cited other benefits of the site in Shelby:

“downstream” from all environmentally concerning areas

not bordered by sensitive Native American properties

only 5 miles due north of STAMP and 11 miles north of NYS Thruway

closer to Niagara Falls hydropower plant

close proximity to major utilities in Medina, including sewage disposal plant

within 2 miles of industrial development facility in Orleans County (Medina Business Park)

seismically stable property

existing 100-acre excavated stone quarry to serve as cooling station for “closed loop” system

located in sparsely population area

limestone material ad concrete plant at location for construction

access to facility on four roads (Route 63, Ryan, Blair and Salt Works roads)

noise less of a factor with currently operating stone quarry

minimal impact on environmental concerns or farming

more amenities available with the village of Medina just comfortably 3 miles to the north

results of reclamation of existing stone quarry

elimination of disposal into Oak orchard Creek

GCEDC said Cardone’s land would be years away from securing the needed infrastructure and approvals to make the site a possibility for such a development.

Johnson spoke about the letter and response from GCEDC after today’s Legislature meeting. She said she supports the development of STAMP but doesn’t want the sewer discharges harming the Oak Orchard Creek, which is a valuable asset in the county, particularly for fishing, the county’s top tourism draw.

The buildout of STAMP would have many positive ripple effects for Orleans County, she said, bringing more residents to the area for housing, businesses and other economic activity.

She said she was aware Cardone was presenting his land as an option for the data center and she said that is his right as a landowner, but it hasn’t formally been presented to the board of the Orleans Economic Development Agency as an option.

Cardone said the land is Shelby is a better location for the data center than STAMP, which borders a Native American reservation and wildlife management areas.

Updated at 11:22 a.m. on Jan. 28

Lynne Johnson, the County Legislature chairwoman, sent this statement about GCEDC’s response to her letter on Jan. 16:

“My job as Chairman of the Orleans County Legislature is to look out for the best interests of our community. In this instance, that means protecting Oak Orchard Creek which, given past history, is why we objected to GCEDC serving as lead agency for the purported data center project at STAMP. Our sole interest is in protecting the natural resources of Orleans County. Any insinuation that we are attempting to poach this data center project is categorically false and a red herring put forth to discount our legitimate environmental concerns.”

By Tom Rivers, Editor Posted 15 January 2026 at 1:36 pm

2 towns together have been billed about $60,000 by Medina last 2 years for ad valorem charges

Photos by Tom Rivers: This photo from Aug. 8, 2016 shows a worker from DN Tanks putting a second coat of paint on Medina’s 3-million-gallon water tank. DN Tank also made several repairs to the water tank that was initially built in 1959 on Route 31A. The tank holds water from the Niagara County Water District. The Village of Medina’s water system also feeds water districts in Shelby and Ridgeway.

MEDINA – The Medina Village Board isn’t backing off collecting money from the towns of Shelby and Ridgeway with their shares of an ad valorem charge from the Niagara County Water District.

The NCWD supplies Medina, Shelby and most of Ridgeway with its water. The NCWD bills Medina about $136,000 annually in an ad valorem charge as an out-of-district user. That charge helps pay for infrastructure and operations of the Water District.

Village Attorney Matt Brooks told the Village Board on Monday it is obligated to collect the ad valorem charges from Shelby and Ridgeway, and may need to take legal action if the towns continue to not pay the bill.

Medina has been bearing the full bill itself, even though a study from 2013 called for Ridgeway to pay 5.02 percent of the bill and Shelby to contribute 17.98 percent. That is their share of the bill based on their water usage back in 2013. (Medina officials expect the towns are using a higher percentage now after adding water districts since 2013.)

Medina, however, didn’t seek to collect the ad valorem charge from the two towns until September 2024.

Shelby was billed $23,554.81 and Ridgeway was billed $6,576.48. Neither has paid.

They were billed again in September 2025, with Shelby’s amount at $23,193.84 and Ridgeway’s at $6,475.70.

The Medina Village Board is determined to get those funds, and will be assessing 10 percent late fees as it does with all of its water customers who don’t pay on time.

Medina Mayor Marguerite Sherman said she has reached out to the town supervisors at both towns to tell them the money is owed, per their contract with Medina. The village sells water to the two towns that comes from the Niagara County Water District.

Sherman said Brian Napoli, the Ridgeway town supervisor, doesn’t think Ridgeway needs to pay. Jim Heminway, the Shelby town supervisor, has asked the town attorney to review the issue, Sherman said.

Village Attorney Matt Brooks advised the board on Monday that the village may need to take legal action if the two towns continue to refuse payment.

“This is an issue of a contractual breach,” he said. “It’s in violation of a contract.”

The Medina mayor said she is trying to reach an amicable agreement with the two municipalities.

“It’s not out of spite,” Sherman said about the bills from the village to the towns. “We want to be good neighbors but we are obligated to collect this amount based on the contract.”

By Ginny Kropf, correspondent Posted 12 January 2026 at 8:36 am

Photos by Ginny Kropf: Andy Benz presided at the installation of officers of the Shelby Volunteer Fire Company.

Orleans County Clerk Nadine Hanlon installed officers of the Shelby Volunteer Fire Company’s Ladies Auxiliary Saturday night.

Hunter Sturtevant, left, and Zach Petry presented David Moden with a chief’s hard hat for his years of service.

MEDINA – Shelby Volunteer Fire Company and Auxiliary welcomed members and guests to their 57th annual installation of officers banquet Saturday night.

Jason Watts served as master of ceremonies, while his father Howard Watts and Auxiliary president Elaine Watts welcomed guests. The evening began with invocation and memorial service by chaplain Karl Haist Jr. Haist reported they had lost six members during 2025 – Tom Fuller, Jim Watts, Fred Filipowicz, Charles “Huck” Fuller, Edward Pray and Elroy Fuller.

The fire company also reported seven new members were added during 2025.

Andy Benz was the installing officer for the fire department. He said he considered the job as an honor.

“A few of the names stick out tonight,” Benz said. “In the past I had given out five chief’s awards and all five of them are still here tonight, and still dedicated.”

Fire company officers installed are president, Kirk Myhill; vice president, Howard Watts; treasurer, Tyler Root; assistant treasurer, Michael Saladeen; secretary, Kali Sturtevant; sergeant-at-arms, Dale Watts; chaplain, Karl Haist Jr.; assistant chaplain, Phil Keppler; and steward, Gary Watts.

Also, trustees – Nick DiCureia, for three years; Ron Smith, two years; and Bill Luckman, one year.

Firematic officers are chief, Zachary Petry; deputy chief, Hunter Sturtevant; assistant chief, Joe Kyle; firematic captain, Marcus Watts; firematic lieutenant, Alex Benz; EMS captain, Jake Quackenbush; and EMS lieutenant, Donnell Bennett.

County Clerk Nadine Hanlon installed Ladies Auxiliary members: president, Elaine Watts; vice president, Brianna Wheeler; secretary, Robyn Watts; treasurer, Lori Myhill; chaplain, Marian Fry; and trustees for one year, Sherry Wheatley; and two years, Mary Herbert.

Elaine Watts, left, president of the Shelby Ladies’ Auxiliary, presented flowers to dedicated members Lori Myhill, Robyn Watts and Marian Fry.

The presentation of special awards began with Howard Watts recognizing David Moden for 34 years of active duty. Moden was also presented with a chief’s hard hat by Hunter Sturtevant and Zach Petry.

Andrea Benz received the President’s Award for stepping up to work on the bylaws and chairing the Christmas party, while completing her teaching degree and planning a fall wedding.

“I can see her being a future president,” Howard said.

The Chief’s Award was presented to Mark Reigle, for consistently leading with his willingness to step up and serve.

Elaine Watts, president of the Ladies Auxiliary, said it was hard to single out one recipient for an award. Instead, she presented flowers to Lori Myhill, Robyn Watts and Marian Fry and announced she would take all the ladies out to eat.

(Left) Howard Watts, left, presents a certificate to Kirk Myhill for 50 years of membership to the Shelby Volunteer Fire Company. (Right) Jason Watts, left, and his father Howard Watts are ready to greet guests at Shelby Volunteer Fire Company’s 57th annual installation of officers banquet Saturday night. Jason served as master of ceremonies, while Howard welcomed guests.

Moden recapped the fire company’s activity in 2025, announcing their 240 calls was fewer than in recent years. Fifty-one percent of the calls were EMS and 16 percent were mutual aid.

Moden also recognized the top 10 responders for 2025. They are Zach Petry, 75% or 181 calls; Moden, 75%; Howard Watts, 67%; Chris Stacewich, 63%; Jake Quackenbush, 52%; Hunter Sturtevant, 47%; Ed Quackenbush, 44%; John Rotoli, 43%; Alex Benz, 41% and Donnell Bennett, 36%.

For his efforts, Petry will receive an embroidered jacket.

“This level of commitment doesn’t happen by accident,” Moden said.

Moden also reported the fire company had received a $95,000 AFG grant last year which will be used to install vehicle exhaust stations. This year they plan to apply for a $300,000 grant to purchase new turnout gear.

Rounding out the evening was dinner catered by The Hilltop in Lockport and music by Beamin’ Sounds.

Members of the Shelby Volunteer Fire Company’s Ladies Auxiliary take the oath of office that was administered by County Clerk Nadine Hanlon.

By Ginny Kropf, correspondent Posted 7 December 2025 at 3:23 pm

OCCS expects to move to location to start next school year

Photos by Ginny Kropf: Krista Lawson, standing, teaches all subjects to first-, second- and third-graders, in addition to teaching Bible and acting as school nurse at Orleans County Christian School. Two of her students are Zavina Wright, 7, and Isabella DeVore, 6. Lawson is the wife of Kevin Lawson, pastor of The Vine Church on Maple Ridge Road.

This is the former Shelby Baptist Church on Allegany Road in Shelby Center. The church, an adjoining cafeteria and a brick building have been donated to the Orleans County Christian School, which plans to start the 2026 school year there.

MEDINA – The Orleans County Christian School is about to make a monumental move, which they hope will propel them far into a successful future.

Now located in Alabama Full Gospel Fellowship Church on South Gravel Road, the church is planning a move to the former Shelby Baptist Church, which has been donated to the school.

“God has opened a remarkable door for OCCS,” said Dawn Zaidel, principal and acting administrator, in a press release last week. “A new building has been donated, positioning us for growth, sustainability and increased community impact.”

“OCCS already has a strong foundation and a rich legacy of faith,” said Ayesha Kreutz, who was recently hired as administrator. “Now we get to be part of the next chapter of this story, strengthening what God began and building toward the future He is preparing.”

The church/school complex in Shelby Center, formerly the Shelby Baptist Church, was donated to the Pastors’ Aligned for Community Transformation (PACT), which donated it to the Christian school.

Orleans County Christian School had its beginnings in October 1993, when the Rev. Tim Lindsay organized a steering committee of individuals with a heart for Christian education. Present were the Rev. Lindsay, Rev. David Vetter, Rev. Randy Anson, Rev. Chris Johnson, Curt Strickland, Curt Follman, Mark Irwin, Vanche Hedley and Dr. William Bellavia.

From that meeting, they sent a county-wide survey to see how much community interest there was. The steering committee continued to meet for three years until, in 1996, the Orleans County Christian School opened its doors on Sept. 4. It began with 13 students, one full-time teacher and one part-time teacher. The school was initially located at Harvest Christian Fellowship in Albion.

After five years, the school moved to Calvary Tabernacle Assembly of God in Medina’s old high school, where they were given use of the northeast wing of the first floor, along with the cafeteria, auditorium and gymnasium. After 17 years there, they were forced to move again when the building was sold, and Alabama Full Gospel Fellowship on Route 63 north of Shelby Center became their new home.

“Pastor Russ Peters and his congregation have welcomed us with open arms, but we are excited about our move once again to a new home,” Zaidel said. “We are also excited about the possibilities for growth at our new location. Orleans County Christian School’s purpose was, and still is, to provide young people with the tools and environment they need to attain the highest level of academic achievement and Christian character.”

Students and teachers frequently gather in the Community Room at Orleans County Christian School. Here, from left, are Mary Hollenbeck, an all-around teacher, GED instructor or adviser on hybrid or distance learning; Dawn Zaidel, principal and English and history teacher; a 10th grade hybrid student; Ayesha Kreutz (standing), newly hired administrator; and students Levi, 13, and Jayden 11.

Zaidel said the school won’t be moving until next September. They have to convert the new church into a dual-purpose gymnasium and community center. The cafeteria is housed in the low wood building which connects the church and brick building on the north, which will house the classrooms.

“It is amazing when God pours out,” Zaidel said. “It’s never something small.”

Kreutz is excited about her new position and what she can bring to the school.

Her background is in classical Christian education, fundraising and organizational turnaround, which she is confident will help strengthen the school’s academics, expand student programs and build on the incredible foundation of this school’s history. As administrator, Kreutz will work as a consultant specializing in grant writing, program development and organizational strategy.

“I bring a blend of administrative leadership, curriculum development, community engagement, fundraising and long-range strategic planning,” Kreutz said. “We are on a mission to keep Christian education alive in Orleans County and investing in a legacy that will serve families for generations. I want to be part of raising up citizens with good character, who have a love of learning, family and community, and are prepared for life, wherever that might lead them. We need to invest in our youth so they will stay here and build this community, not just leave the first chance they get.”

Sophia Standish, standing, is working with Abigail Smith, a new student at the Orleans County Christian School.

The Orleans County Christian School is supported by Harvest Christian Fellowship, Albion; Calvary Tabernacle Assembly of God, Medina; Faith Alliance Church, Albion; First Baptist Church of Holley;

Oak Orchard Assembly of God and Alabama Full Gospel Fellowship, Medina; Light of Victory Church, Albion; and Faith Covenant Fellowship, Medina.

The parent of a former student shared this testimonial: “This is an awesome school that takes time for one- on-one learning and really cares about the kids. My daughter has gone there for almost 7 years.”

The Orleans County Christian School accepts children from pre-school through 12th grade. This is the first year for preschoolers and they are filled to their capacity of seven children.

Michael Zaidel, school nurse and member of the Christian school board, said most parents don’t realize they can get busing to and from our school if they live within 15 miles of the school. They currently have students registered from Royalton/Hartland, Albion, Holley, Oakfield, Lyndonville and Batavia. Several students are driven in by their parents, he said.

The school is also able to offer students participation in BOCES, and busing is provided, Dawn Zaidel said.

The school plans to use the brick building on the north for the classrooms. The church building is planned to become into a dual-purpose gymnasium and community center. The cafeteria will be housed in a low wood building which connects the church and brick building.

Kreutz said they are looking at additional opportunities for students at the school.

“The kids want to start a Club America,” Dawn said.

“It is student-run and encourages kids to develop different service projects in the community,” Kreutz said.

Dawn said when she was asked to fill in as administrator, the first thing she did was brainstorm on how they could get more students enrolled.

“We have gone from eight to 20 students,” she said. “Our capacity is 37. I am a firm believer if we can get a child from the beginning, he will stay. Our parents are overjoyed we are able to now accept preschoolers.”

The Orleans County Christian School depends heavily upon donations, and anyone wishing to donate to the school may make a one-time donation of any amount or pledge a monthly gift by logging on to www.orleanscountychristianschool.com; or mailing a check to OCCS, P.O. Box 349, Medina, 14103. Donations can also be made through Venmo:@occsschool.

Pictured from left include Garner Light, Melissa Mance-Coniglio, Emma DeLeon and Betsy Black.

Press Release, Friends of Iroquois National Wildlife Refuge

MEDINA – At its annual meeting Nov. 22, the Friends of Iroquois National Wildlife Refuge elected a new member to its board and officers for the coming year.

Elected to the board was Garner Light of Gasport, the group’s past president. Emma DeLeon of Williamsville was re-elected vice president, Betsy Black of Lockport was re-elected treasurer, and Melissa Mance-Coniglio of Bergen was elected secretary.

“Congratulations to those elected by the membership,” said the group’s current president, Richard Moss of Medina. “I look forward to collaborating with them on initiatives like our popular eagle nest camera.”

Friends of Iroquois National Wildlife Refuge is a 501(3)c nonprofit corporation that exists to support and enhance the 10,800-acre Iroquois refuge, operated by the U.S. Fish & Wildlife Service. The nonprofit’s main goals are public education, visitor services, and wildlife protection and management.

Community turned out Saturday in big benefit for Hodgins family

Photo by Tom Rivers: Michael Hodgins is shown Saturday in the Shelby fire hall where the community packed the building for a spaghetti dinner and basket raffle in his honor to help the family with expenses for his second heart transplant. Hodgins had his first heart transplant 35 years ago.

By Tom Rivers and Ginny Kropf

MEDINA – Michael Hodgins got his new heart Wednesday morning. Hodgins has undergone successful heart transplant surgery for the second time.

The first time was 35 years ago. The community had a big benefit for Hodgins and his family on Saturday at the Shelby fire hall.

Hodgins, 64, was on the list for a heart transplant at the Cleveland Clinic, but the exact date for the surgery couldn’t be known.

On Tuesday, his family got the call at 1:30 p.m. that a heart was available.

He was in Cleveland and headed in for surgery at 10 p.m. that night. He received the new heart at 4 a.m. on Wednesday, his daughter

went in for surgery 10 p.m. on Tuesday with new heart in at 4 a.m. Wednesday, his daughter Alisha Duffina posted on Facebook.

“Michael Hodgins is so resilient and strong!!” Duffina posted on Facebook on Thursday. “Doctors are very pleased with his recovery and he possibly will be ready to graduate to a step down unit tomorrow! Thank you for your continued love and support!”

Hodgins first had a successful heart transplant when he was 28. He had that surgery at Buffalo General and it was a tremendous success giving him 35 more years of life.

Hodgins had a failing heart at age 27. He was born a preemie, just over 2 pounds and had a hole in his heart. He had heart surgery at age 9, and seemed to be doing OK until he was 27.

After more than 20 years with the Jubilee in Medina, he needed to get a new job when the store closed in 2006. Hodgins then joined Medina Memorial Hospital and works in the dietary department at the hospital.

He and his wife, Kathy, have three grown children and seven grandchildren.

By Tom Rivers, Editor Posted 16 October 2025 at 10:18 am

Carl Zenger wins national award for 22 years of dedicated service at Iroquois National Wildlife Refuge

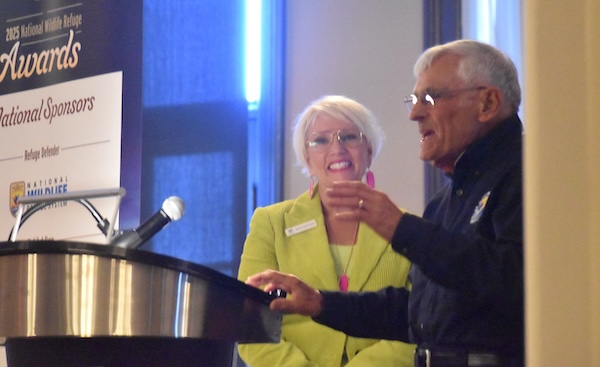

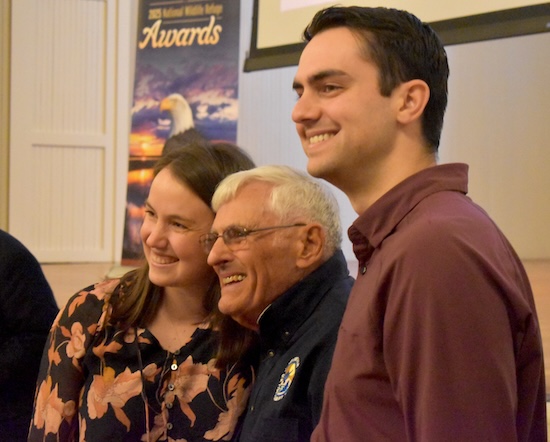

Photos by Tom Rivers: Carl Zenger holds up a certificate of commendation he received on Wednesday from a staff member for Congresswoman Claudia Tenney. Zenger received 2025 “Refuge Volunteer of the Year” award from the National Wildlife Refuge Association. Zenger has been a full-time presence at the local refuge for the past 22 ½ years.

MEDINA – There are 570 national wildlife refuges in the United States and many dedicated volunteers have been critical to educating the public, maintaining grasslands, nurturing wildlife and serving in other roles.

Of all the volunteers in the refuge system, Carl Zenger stands out among them all for his dedication at the Iroquois National Wildlife Refuge, which covers 10,824 acres in the towns of Shelby and Alabama.

Zenger, 87, is up at 5:30 a.m. every day and make the 20-minute drive from Lockport. He is at the refuge by 7, typically the first one there.

He has kept a full-time presence at the refuge the past 22 ½ years, amassing 45,000 hours of volunteer service.

Zenger delights in mowing about 200 acres of grasslands each year, and along miles and miles of drainage dikes. He was instrumented in starting the Friends of Iroquois Wildlife Refuge in 2000, and has served as president, vice president and board member. That organization raises about $15,000 to $20,000 a year to support the refuge. Its fundraising has helped rebuild the Swallow Hallow Trail, extend the Cayuga Overlook Platform, install an accessible floating dock at the Ringneck Marsh, and sponsor youth fishing derbies and waterfowl hunts.

Tom Roster, the retired manager of the Iroquois National Wildlife Refuge, spent just over 20 years with Zenger at the refuge. Roster praised Zenger’s commitment to the refuge and his willingness to serve in many roles at the site.

“Carl is a person of many talents,” said Tom Roster, who recently retired after more than 20 years as the refuge manager. “His volunteering has touched all aspects of Iroquois National Wildlife Refuge daily operations including habitat management, wildlife population monitoring, maintenance, interpretive and educational programs, outreach and yes, we even got him to do some administrative work. We just didn’t call it that. We referred to it as safety or vehicle and facility maintenance!”

Roster was among about 100 people who celebrated Zenger and his distinguished award as national volunteer of the year during a luncheon on Wednesday at the Bent’s Opera House. Many other dedicated local refuge volunteers and staff attended the luncheon. (Due to the federal government shutdown, the refuge staff attended in regular clothes, not their refuge work attire.)

Zenger grew up on a dairy farm in Pennsylvania and worked 42 years at General Motors. When he was nearing retirement from GM, he looked for a way to stay busy and give back to a worthwhile organization. The refuge was a perfect fit, utilizing his talents at a site with a long to-do list.

Carl Zenger said he has a great relationship with the refuge staff and other volunteers. “I did it because I wanted to be there,” he said about his volunteerism at the refuge.

Some of the projects Zenger has spearheaded, outside of routine maintenance, include:

• One of his first projects was establishing a bluebird trail with over 50 bluebird boxes along the trail. Zenger still coordinates the maintenance of this trail and has taught dozens of other volunteers and interns how to maintain the boxes, manage the program, monitor and band the birds.

• Zenger has worked to expand birding programs to include other cavity nesters like swallows, kestrels and purple martins.

“Carl’s interest in Kestrel grew as he saw that kestrel populations decline by 85% in New York State,” Roster said. “Carl has provided guidance on where and how to put up kestrel boxes on the refuge including switching over to his own pulley system that assists in lowering and raising nesting boxes for monitoring, thus eliminating the need for climbing up and down ladders. He ensures that monitoring is conducted every year.”

Those birding programs resulted in 130 bluebirds being fledged in the past year, 352 tree swallows and 71 house wrens, Zenger said, praising the refuge staff and volunteers. “Great job!” he declared from the podium at Bent’s Opera House.

Zenger is presented with the 2025 Refuge Volunteer of the Year Award by Wendi Weber, a board member for the National Wildlife Association and retired regional director for the U.S. Fish and Wildlife Service.

After the success of the bluebird trail, Zenger shifted to establish a purple martin colony at the refuge. Carl worked diligently for several years before he started to see any response to his efforts, Roster said.

“Each year he would put out purple martin decoys and play the ‘dawn song’ to hopefully attract any lost martins that happen to be passing by,” Roster said. “There were finally a few takers, and over the years that has grown to multiple colonies on the refuge that annually produces over 700 fledglings.”

One colony is adjacent to the parking lot at the refuge headquarters, and provides a great opportunity to educate refuge visitors on conservation of the species and show the bird monitoring and banding techniques very easily, Roster said.

Zenger makes the added effort of ensuring that calcium is available to female martins that may be deficient after laying a clutch of eggs.

“He collects eggshells from his local community breakfast event, rinses and bakes them to remove any potential salmonella,” Roster said. “He then crushes them and adds them to feeders at twelve sites where purple martin females can obtain this essential mineral that is integral to their post laying condition survival.”

This year, there were a record 950 purple martins banded at the refuge and 700 fledges.

Zenger said he prefers to be low-key and out of the spotlight. But his dedication over so many years stands out – across the country.

He thanked the staff and other volunteers, and especially his family, including his late wife of 63 years, Phyllis. She often joined him at the refuge for projects, working in the welcome center and with public education programs.

Zenger is eyeing a goal of 50,000 hours of volunteer service at the refuge.

“If it’s God’s will,” he said about continuing as a very active volunteer. “I’m not quite done yet, but I may have to temper my pace a bit.”

Desirée Sorenson-Groves, president and CEO of the National Wildlife Association, congratulates Zenger on his award. Sorenson-Groves, who is based in Washington, D.C., said refuges across the country have seen a gradual reduction in their workforces over the past decade. Iroquois, for example, used to have two full-time maintenance positions that haven’t been filled.

“The way things are going, volunteers are the future of maintaining our refuges,” she said.

Zenger is joined for a photo with his grandchildren, Malia Keespies, left, and Mattison Zenger Hain.

By Tom Rivers, Editor Posted 11 October 2025 at 10:08 pm

Shelby fire hall packed for spaghetti dinner, basket raffle

Photos by Tom Rivers

SHELBY – Mike Hodgins, left, is greeted by Matt Grammatico of Albion today during a big benefit for Hodgins as he awaits a second heart transplants.

Hodgins, 64, had a heart transplant 35 years ago. He is on the list for another heart transplant at the Cleveland Clinic.

Grammatico, 52, of Albion is nearing the fifth anniversary of a heart and liver transplant at the Cleveland Clinic. Grammatico received those transplants on Jan. 12, 2021.

Grammatico and Hodgins have been friends on Facebook for several years and have been cheering each other on through social media. Today they met in person for the first time.

“I don’t want to miss the chance to connect with another heart transplant recipient,” Grammatico said.

The community also put on a benefit for him and his family before his transplants. He was thrilled to see such a big turnout today for Hodgins at the Shelby Fire Hall.

Hodgins said he and Grammatico are both miracles who have been given another chance at life by God’s mercy. Hodgins is wearing a “Miracle Mike” shirt.

Mike Hodgins takes a brief break from greeting friends, family and community members who attended a benefit for him and his family today.

“I’m just overwhelmed,” Hodgins said.

He and his wife Kathy have three children – Alisha, Greg and Ryan – and seven grandchildren.

Mike and Kathy need to travel about four hours to the Cleveland Clinic for testing, evaluation, surgery and recovery. This will require extended time away from work and significant out-of-pocket expenses for lodging, food and transportation.

“I’m taking it one day at a time,” said Hodgins, a longtime employee at Medina Memorial Hospital in the dietary department. His wife is chief executive officer at UConnectCare.

There were 200 people at the fire hall within the first hour of the benefit which was 4 to 8 p.m. today. There were 195 baskets up for raffle, plus 86 gift cards.

Businesses from the region donated gift cards as part of today’s benefit which was led by Hodgins’ niece Stephanie Kozma.

Many family members, friends and members of the Oak Orchard Assembly of God rallied to run the benefit.

Dark Horse Run entertained the crowd with country music.

Some of the kitchen crew serving spaghetti dinners included, from left, Julie Mufford, Pete Panek and Amy Albone. They had 400 dinners ready.

The Shelby fire hall was a full house for the benefit.

Matt and Rhonda Grammatico of Albion pray with Hodgins as he awaits a second heart transplant.

By Tom Rivers, Editor Posted 9 October 2025 at 5:24 pm

Photo by Tom Rivers

EAST SHELBY – A fire caused extensive damage this afternoon inside a house at 12491 Smith Rd.

Firefighters were dispatched to the scene around 3:30. No one was home at the time of the fire. A family of three lives there in a house owned by Douglas Watson.

The family’s dog perished in the blaze. The fire in under investigation and the cause is undetermined at this time.

Multiple firefighters joined east Shelby in responding to call. The fire caused extensive damage to first and second floors, and the attic.

Zack Petry, deputy chief for Shelby, is on the ladder trying to vent the house from smoke.

Firefighters set up a dump tank for an added supply of water. This is a rural area in southern Shelby near the refuge where there aren’t fire hydrants.

By Tom Rivers, Editor Posted 8 October 2025 at 10:26 pm

EAST SHELBY – The Orleans County Emergency Management Office is advising the public of an oversize load on Thursday morning that will go from Knowlesville to East Shelby.

The load will make its journey starting at about 6:30 a.m. from Growmark FS. The load will go south on Taylor Hill Road and Townline Road, making its final destination to East Shelby Road.

“Due to size and slow speed, we encourage those in the area of transport to use caution,” the EMO stated. “And for morning commuters, alternate routes are encouraged.”

By Ginny Kropf, correspondent Posted 23 September 2025 at 8:45 am

Photo by Tom Rivers: A group walks down East Shelby Road on Oct. 7, 2023 for the 35th annual walk/run for the Knights-Kaderli Fund. The Knights and Kaderli families estimate that more than $1 million has been used from the fund since it was established, helping cover some of the utilities, co-pays and other bills for people fighting cancer in Orleans County.

MEDINA – For the past 37 years, the community has gathered for a walk/run to support patients living with cancer in Orleans County.

The Knights-Kaderli Walk/Run began when two families – those of Richard Knights and Sue Kaderli – decided to join their fundraising efforts in memory of their loved ones into one event.

“This year we are happy to celebrate our 37th annual Knights-Kaderli Walk on Oct 4,” said Stacey Knights Pellicano, Knights-Kaderli board member and daughter of Richard Knights. “This is our favorite time of year. We look forward to being with all of our supporters. If you have ever participated in our event, you understand the energy of that day. It gives us hope and unites participants.”

The walk/run will begin at 11 a.m. Oct. 4 at East Shelby Volunteer Fire Hall. Registration fee is $20 and participants are encouraged to ask their friends and neighbors for small sponsorship donations. Every dollar helps, Pellicano said. There is also a large basket raffle for the Knights-Kaderli Fund that morning at the East Shelby Firehall.

The 5K will continue as an untimed walk/run, so registrants can participate in a leisurely walk with family and friends, or set their watches for a 5K run. As always, participants and the community are encouraged to participate in their basket raffle. Lunch will be served immediately after the race and guests may eat outside under the pavilion. Everyone is urged to photograph their experience and tag Knights-Kaderli on Facebook and Instagram at #KnightsKaderli5K for some fun prizes.

Richard Knights and Sue Kaderli were both lifelong residents of Orleans County. Knights died from cancer at age 38 in 1984. Kaderli passed away from the disease at age 52 in 1989.

“They were both known for their spirit of community and we are honored to remember them in this way,” Pellicano said.

Funds are raised through annual events and various contributions made by individuals, organizations and memorials.

For more information or financial assistance, contact Mary Zelazny at (585) 746-8455, Melissa Knights Bertrand at (716) 983-7932 or Pellicano at (716) 998-0977.

Participants may register for the walk/run online (click here). Those unable to participate are asked to consider a direct donation through Venmo@knightskaderli.